Investors looking at high yield property valuations need to focus on real income, risk, and market fundamentals — whether considering NDIS or co-living opportunities. They often ask the wrong questions. “What did he pay for the land?” “What was the build cost?” “Why is he selling if it’s so good?” These questions might feel logical, but they often miss the mark. To make smarter investment decisions, you need to focus on what really matters: what is the property worth now, and what income does it generate?

Let’s clear some things up — using the numbers.

The Value Is in the Income, Not in the Finishings

A beautiful home with premium fittings might impress an owner-occupier, but that’s not who you’re selling to. In NDIS or co-living property, buyers aren’t swayed by gloss — they’re guided by returns.

If your investment is producing a solid, consistent income, it will hold real market value. If not, no amount of marble benchtops will convince an investor otherwise.

“But Why Is He Selling If It’s Performing So Well?”

Smart investors sell a performing asset when the value is highest. They wait until it’s tenanted, generating income, and has a clear valuation path. That’s when it offers real value to a buyer — and that’s when they can be rewarded for the work they’ve done.

If a product isn’t performing yet, most experienced investors will hold it, fix the problem, and only sell once it’s stabilised. Selling while it’s underperforming is not ideal. It’s like selling stocks in a dip and holding onto the losers — it’s bad business.

So if you’re thinking: “If it’s so good, why is it for sale?” — consider this: you don’t always buy from someone who failed. Sometimes you’re buying from someone who knows how to build value and is ready to harvest it.

“What If the Property’s Been Vacant for a Year?”

If an NDIS property has been sitting vacant, it’s not necessarily a bad property — but it’s not a proven one either.

The issue could be a poor SDA provider, a lack of active tenancy strategy, or a mismatch between the design and demand. There are many underperforming SDA properties, but many are struggling due to bad management and a passive approach not bad design. We’ve seen this time and time again.

But even with reasons and excuses, the market sees it as unproven — and buyers will demand a discount for taking on the risk.

If you’re asking someone else to wait 12–18 months or fix all the problems, they should be rewarded for that.

We’ve taken on properties in oversupplied or underperforming areas, turned them around, and achieved strong outcomes — but that doesn’t mean they were worth full price when we bought them. The discount reflects the risk.

Co-Living Doesn’t Have the Same Vacancy Risk

Co-living properties generally gets fully filled within a matter of weeks. And even if one room is empty, the others still earn income. That’s a key strength. So the risk level is different, and so is the valuation logic.

“Can’t I Just Build It Cheaper?”

Yes, you can build it cheaper — if you’re willing to take on the project.

But that’s the point. If you’re project managing a full build, sourcing the land, managing builders, and handling the compliance process, you are creating value through risk and effort. That’s where you make your money.

Buying a completed product means you’re paying for someone else doing that work. That’s not a bad thing — but don’t expect to pay the same as raw land and build cost. You’re buying a final product, not a project.

“At the End of the Day, It’s Just a House” – No, It’s Not

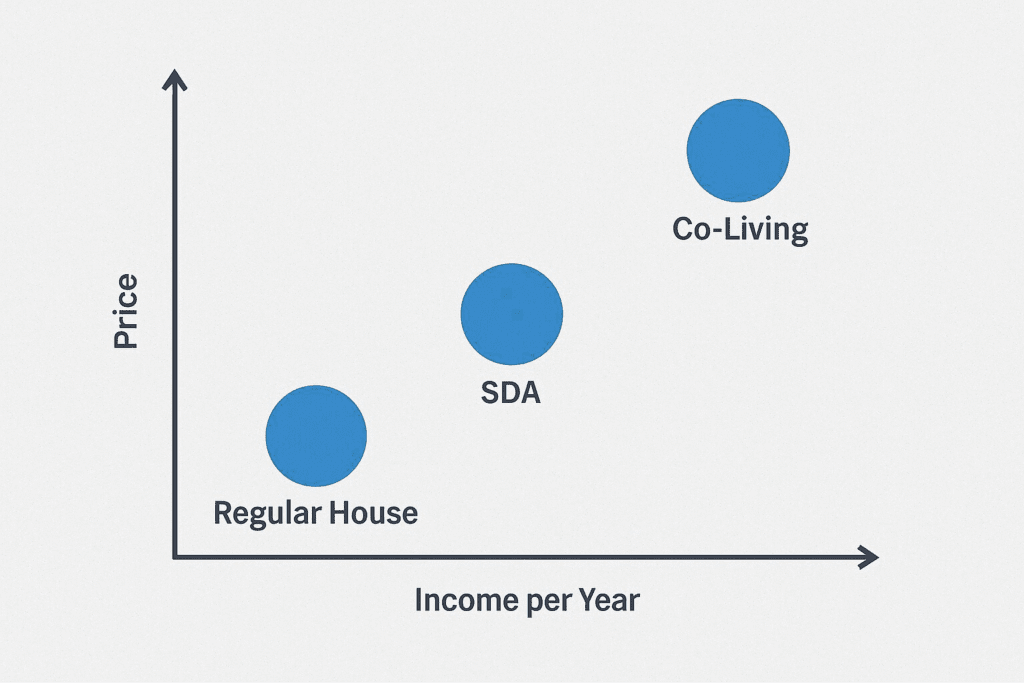

If you (or your broker for that matter) are comparing a co-living investment to median house prices in the area — you’re completely missing the point.

A regular home might earn $25,000 per year in rent.

A purpose-built co-living could bring in $160,000+.

They’re different vehicles entirely.

That’s like saying a Ferrari is too expensive because a Fiat is cheaper.

“What Was the Land Price? What Did the Build Cost?”

This is the wrong question. Why?

Because it doesn’t matter what the seller paid two or three years ago. It matters what the land is worth today and what the build would cost now — if you could even replicate it.

And let’s be honest — why are you so afraid of the other guy making money?

You won’t trick a sophisticated developer into giving you a bargain. They do this to make a profit. That doesn’t make it a bad deal for you. The goal is a win-win, not a trick deal where you somehow steal value.

If someone is selling you a completed, tenanted, high-income asset, and you’re holding out because they made money — you’re missing the opportunity in front of you.

“But the Commercial Valuation Is Higher Than the Sale Price!”

Yes — and that’s often a good thing.

A commercial valuation is based on rental income and yield, and it’s useful for financing. But if the gap between sale price and valuation is too big, something’s off. Either the income is inflated, or the market just doesn’t accept that price.

There’s a balance. A completed product is worth more than a raw project, but not always worth top commercial valuation. The valuation gives you equity and leverage.

“I Think It’s Not Worth That Much – I’ll Just Offer 200k Less”

You can try, but good luck.

Top-performing properties aren’t the place to look for discounts. If it’s tenanted, producing strong income, and priced in line with what the market is paying — it will sell. If you underbid because “you feel” it’s worth less, don’t bother, someone else will buy it.

Are you after value, target high-risk, untenanted, underperforming assets — but know what you’re taking on. That’s not a bargain — that’s a risk assessment.

Equity Uplift vs Capital Growth

One of the most misunderstood ideas is that high-yield investments offer poor growth.

Not true.

Equity uplift from increased rent is often much more powerful than passive capital growth.

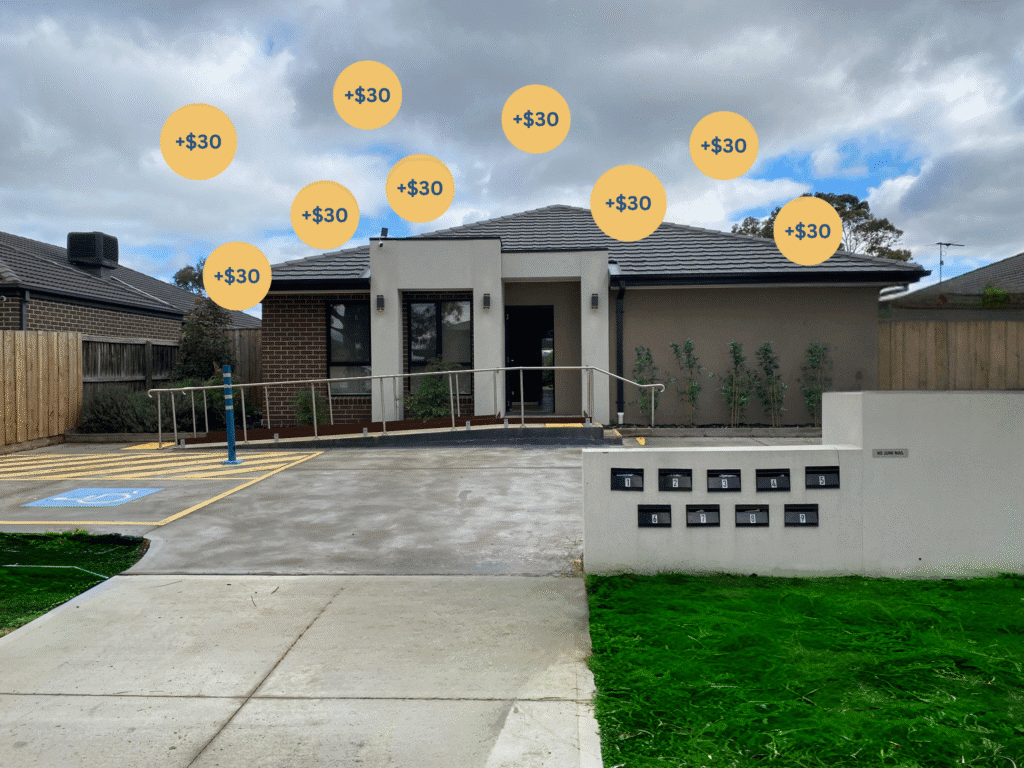

Example:

Raise your rent by $30 per room across 9 rooms →

That’s $14,040 extra per year in income.

Multiply by a cap rate of 6% = $234,000 valuation uplift — without any land value change.

This is how serious investors grow their portfolios. Not by waiting for the market to move, but by creating value.

Focus on Strategy — Not Emotion

Every investor has a different goal. Some want capital growth, some want yield, some want long-term stability. But don’t compare different strategies and expect the same pricing model.

A performing NDIS or co-living asset has measurable results. If you’re not ready to act when you see a good one, someone else will be.

Final Word: Understand the Asset You’re Buying

If you’re investing in NDIS or co-living, you need to stop thinking like a homebuyer and start thinking like a business owner.

Understand:

What you’re buying

Why it’s priced the way it is

What the valuation represents

Are you prepared to do the work or pay for someone else who already has

Written by Asle Kommedal

Topstone Property Invest